Imagine you’re on a credit team - your job is to define the credit policy. Risk Management tells you to cut back on approvals to maintain a loss rate target. Marketing tells you to increase approval rate to boost ROI. Collections tells you to reduce lines to minimize $ losses.

Everyone is optimizing their own metric - and everyone is right.

The problem is, none of those metrics answer the question that actually matters: does this decision create long-term value?

Finding an objective function

Lenders in the modern world face a myriad of decisions to make throughout the lending lifecycle. To make these decisions, organizations need a common objective function to assess the impact of changing or implementing a strategy. Having an effective objective function ensures that initiatives are compared apples-to-apples, serves as a communal language for the organization, and encourages a balanced viewpoint of a decision’s benefits and costs. Common objective functions include Return on Assets (ROA), Return on Equity (ROE), Return on Ad Spend (ROAS), Internal Rate of Return (IRR), Net Present Value (NPV), and payback period. Whether making decisions on underwriting, line management, fraud rules, collections strategies, marketing optimizations, or releasing new products, using one of these functions allows the same lens to be applied when analyzing the impact of such changes.

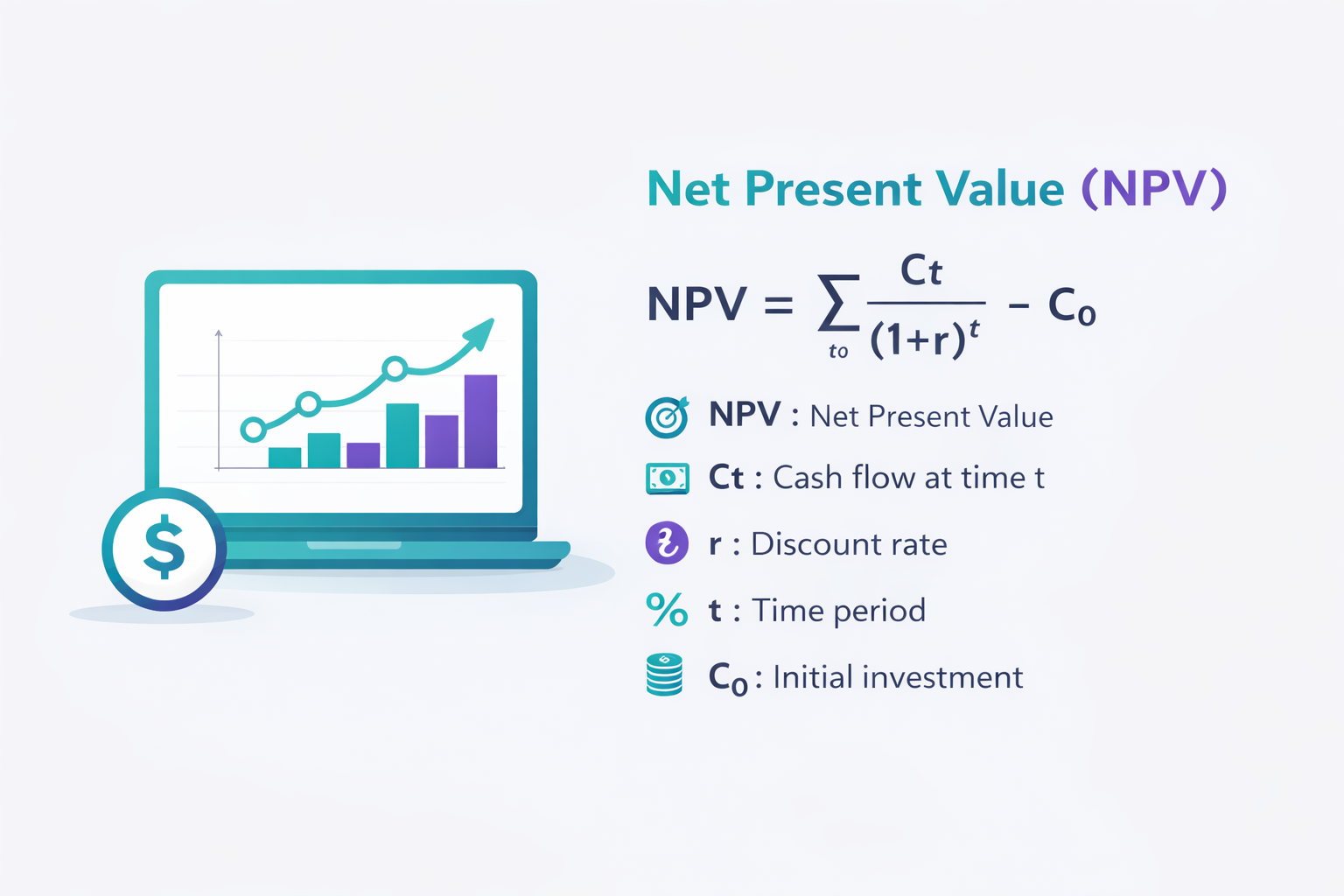

What is NPV?

NPV, or Net Present Value, is the current (discounted) value of cash inflows and outflows over the lifetime of an income stream. Businesses across many industries use NPV to assess the profitability of an investment or company, while more advanced organizations apply it at the individual customer, product, or project level. NPV can be used both to understand current lifetime value (e.g., of a customer), and to evaluate different scenarios and strategies. By calculating NPV for each business decision and comparing the variance caused by a strategy change, we can estimate the impact of any material change.

Why is NPV the gold standard?

While other objective functions can be used in a decision-making framework, Net Present Value is considered the gold standard because it:

- Considers the full P&L

- Accounts for the time value of money

- Allows for cash flow adjustments

- Evaluates full lifetime value of an account or treatment

Capturing the full P&L ensures that both the costs and benefits of each decision are incorporated, encouraging a disciplined view of all of the elements of the business.

It is especially important in lending to take into account the time value of money due to the asymmetrical nature of the cash flows in products like a traditional loan. These loans involve large initial cash outflows when the loan is disbursed and capital reserves are built, followed by small payments and capital releases over the loan’s term. A loan with a short term or higher starting payments will be more profitable than one that is longer term, all else equal, due to the opportunity cost of lending out the funds.

Evaluating the full lifetime value of an account or business ensures that the totality of the decision is captured, rather than a short-term view.

Incorporating all these elements ensures that all available information is considered when making a decision in a quantitative manner.

Granular and Gameable

NPV models should be modular and can be as simple or complex as necessary for the scope of analysis being undertaken. The mechanics (“shell”) of an NPV model remains the same, but the inputs will differ across functions like credit, product, and operations, as well as in the level of complexity of forecasting. They can be designed to measure Life-Time Value (LTV) at a granular, individual level, or at a high level for an entire company. They can also be gamed by running scenarios to determine how LTV will change given different treatments to the underlying inputs.

For example, you may want to evaluate the impact of an adjustment to your credit limit increase program. To do so, you would first calculate the base NPV assuming the current strategy. Next, you would need to determine adjustments to the inputs that a new credit limit increase program would impact, such as credit line, utilization, revolve rate, and loss rate. Ideally, these adjustments would be grounded by testing or inference from available data points. Once the new assumptions are added to the model, you generate a new NPV, allowing you to run different scenarios (i.e., different credit line increase amounts) to understand how sensitive your program is to specific changes.

How to Build an NPV Model

- Define the unit of analysis (customer, account, segment)

- Early alignment on the model’s granularity is imperative for setting up the correct structure and collecting the necessary data.

- Collect inputs (e.g., corporate drivers, performance data, P&L data)

- Often, organizations lack performance data structured correctly for this type of analysis or do not have an internally aligned discount rate.

- Forecast key drivers (e.g., balance, purchase volume, eAPR, utilization)

- Correctly forecasting drivers is the most important and difficult part of the build, requiring a high degree of rigour and sound judgement.

- Model cash flows over time

- The “calculator” converts the model drivers into expected cash flows.

- Ensure alignment with corporate constraints such as taxes, capital reserves, and discounting

- Line items outside of NIBT need to align with corporate assumptions.

- Validation

- Model validation can be completed by comparing predicted cash flows to actuals at a segment or portfolio level.

- Run sensitivity analysis

- Performing sensitivity analysis helps identify which inputs are most impactful to NPV and may require more precision.

- Deploy the model

- Utilize the NPV calculations to implement the model as part of the decision making flow and design policies and strategies.

- Develop monitoring

- Essential to making smart decisions is ensuring model performance does not degrade, evidenced by performance drift from modelled predictions.

Common Pitfalls

- Choosing the right reference data: strategies change all the time, and it is imperative to choose data that best reflects expected future performance

- Ignoring second order effects: changes to inputs rarely occur in isolation; often other drivers are affected (e.g., increasing pricing may result not only in fewer customers being attracted to your product, but also in the remaining customer base being disproportionately higher risk)

- Poor segmentation: inadequate segmentation can hide key insights into specific segments that are high risk or high value

- Monitoring and maintenance: failure to consistently monitor and adjust model predictions to current market conditions and behaviours will lead to model degradation

Payson’s data-driven approach

The best NPV models are data-driven, built on a mix of historical data and adjustments based on planned strategy changes or exogenous factors. Payson specializes in helping organizations build accurate and granular predictions by developing cash flow forecasts from their data, rather than the P&L. By utilizing past indicators and expert judgement, we establish behavioural models that serve as inputs to cash flows. This allows us to fine tune assumptions to ensure that future behaviour is accurately predicted.

Payson also provides guidance on integrating NPV-based decisioning into your strategies. We’ve helped clients across multiple products optimize areas such as credit and risk strategy, line management, collections, product development and pricing, fraud and marketing. We don’t just build models - we ensure that teams are brought along in the process of building the models’ infrastructure and have the tools to make the most of this decisioning framework.

In an increasingly complex lending environment, intuition and isolated metrics are no longer sufficient. NPV provides a unified, rigorous framework to evaluate decisions across the lifecycle - ensuring that growth, risk, and profitability are aligned.

Organizations that unlock their data and operationalize NPV-based decisioning don’t just make better decisions - they make them consistently.